The SEC tries to fend off investors from trading risky assets. It can be anything from OTC stocks to cryptocurrency (but not Bitcoin ETF since recently) to crowdfunding. And while investors have a vague comprehension, they are almost completely ignorant of private equity.

“It’s something for pro-market players,” a typical Reddit user would tell you. Indeed, there are more questions than answers. They could not be found so easily without opening a book or stepping through the door of the industry. It’s hard to value a private company that has limited information. It’s hard to sell fast when most needed. No screeners, no statements, no coverage. Okay, let’s skip this idea and buy an already tripled chip-to-AI company to fuel the growth even more. Oh, and hope to sell it to someone even more enthusiastic before things go in the wrong direction.

During the last 40 years, the proliferation of aggregated publicly traded financial data from numerous providers has made it extremely hard to find bargains without being in the industry. Now it’s not enough to know that Coca-Cola is delicious and that people will buy iPhones in the future (will they?). Moreover, you need to be the first one to spot a young company in a garage that’ll grow fast.

In his book, 100 Baggers, Christopher Mayer tells us that investors need to catch the wave while it’s small and ride it like a pro surfer to 100x. All this sounds plausible until you realize that only 90 companies have delivered more than half of the total stock return over T-bills between 1926 and 2016. And if selecting a winner would be the only problem!

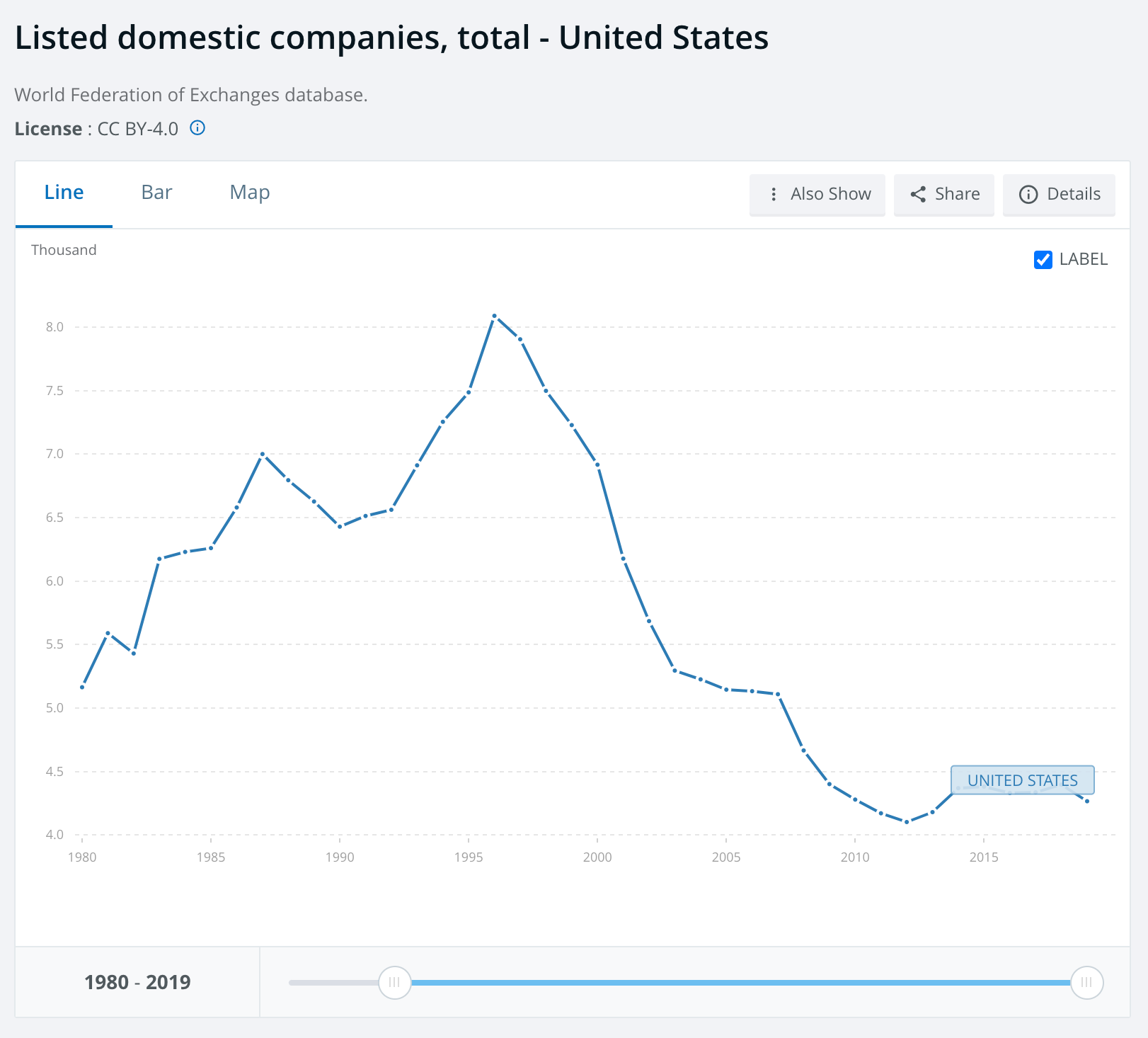

The pond is decreasing too. The number of publicly traded companies decreased significantly from the pick of 8090 companies in 1996 to 4266 in 2019.

Back then, an IPO was considered a way of attracting capital to grow bigger, not an exit for investors. Small bakery chains could easily go public and grow twice as fast compared to taking credit from a bank. But then the 2% inflation target and almost zero interest rates made it a no-brainer choice where to get the money. Luckily, many investors now realize that money is sometimes free and can sometimes cost you 20%.

As I specialize in the tech industry, I’ll show you the inner kitchen of the startup soup. Usually, venture capital funds (a subcategory of private equity) lock investors' money for 10 years. Invest them in a bunch of startups, and pray that one or two of them will become unicorns and go public. Five of them will be okay and will be sold to private equity funds or competitors The rest will be thrown away. All that work will be to underperform the S&P 500.

Why not sell the stocks of the okayish companies to the IPO too? That’s a wonderful question! The harsh truth is that if they do this, they’ll lose money. The moment the company raises its A or B round (the usual pre-IPO round), the valuation is already so overblown that the only way to make ends meet is to pass it on to someone who’ll pass it on to someone who’ll, you know.

Why do VC companies have high multiples? Well, when private equity funds measure the price of a business, they use any human-kind possible metrics, except generated cash. Potential revenue, user growth, number of locations, preliminary contracts, and happiness of customers. All that can work as long as 1) rates are lower or the same as during the last round so that you can raise money with a higher multiple, and 2) you stay inside the private equity market. The day a company goes to a public market, the charm is over, and millions of capital allocators will measure the cash return on hard investment.

And while VC is the world on its own, what’s on the east coast? Established private businesses with moderate to no growth have just two ways of being sold. Either to a private equity fund or a competitor for consolidation. Alright, there’s a third. Synergy. It is a glamorous way to spend money when a business has free cash flow, but just paying dividends will make the CEO look like a rookie in the business world. “Let’s unload 5 years of retained earnings to buy the 2% margin truck services to save on repairs” is the classic example of illusory business synergy. There’s nothing better than a customer expensing someone’s money instead of spending its own.

Investing in private equity may be something that feels hidden from the eyes of investors because this is where the real money is made, as they think. Yes, you can make money in the inefficient private market. Like in the public market 50 years ago, when it was less efficient than it is today. Yes, the flow of new companies is dwindling, and private ones prefer to stay that way longer. But how do you start if you’re not an equity fund manager and not a venture investor who can afford to invest in 10 startups at once?

There are off-market, little-known, family-owned gems, like a retiring owner or a little candy shop, that you and all your neighbors admire. You can buy those businesses. And it’s private equity investing too, without all those suits and pitch decks. There’s a saying I like: “Good companies are bought, not sold,” although people try to prove this to be wrong. But people also say the market is efficient.

Don’t frame yourself. If you feel like the public market is dry (I should’ve published this when the interest rates were 0.5%), try to look for good businesses everywhere. Investing in perfect companies for a good price shouldn’t end when there’s no stock ticker.

An excellent overview in the way of private equity. Business models can be very profitable at some point and make much less sense under different circumstances.

The hike of rates from 0-ish to 5% is case in point, and may drive some defaults.

The SEC has certainly been active in trying to protect retail investors from highly risky or obscure areas of the market. It’s easy to understand why when you consider how many people dive into things like OTC stocks or certain cryptos with very little knowledge. Even with the recent green light for Bitcoin ETFs, the rest of the space is still largely a grey area for newcomers. Crowdfunding platforms have opened up access, but many don’t fully comprehend the risk-return dynamics. What’s even more obscure for the average person is private equity. Unlike traditional markets, it operates in a world of its own, often with limited disclosure. Most investors have only a faint idea of how it works or why it’s reserved for certain participants. The SEC clearly has a challenging role in trying to balance innovation with protection. At the end of the day, understanding these niches is vital before putting any hard‑earned money at risk.

https://comparebrokeronline.com/top-10-commodity-brokers-in-india/